Choices of interest rates

365/24x7

Free of cost advice

Reverse mortgage - Take true value of your home for a safe future

A reverse mortgage is a workable method to secure your future at the retirement age with no dependency on others. Use your equity to fulfil your financial goals with ease through workable mortgage options that Shine Mortgages bring to you from our wide panel of reverse mortgage lenders. We commit to making things easier for you through a team of experts. From mortgage application to documentation and fund disbursement, we take care of everything.

How does a reverse mortgage work?

Reverse mortgage lets you turn the value of your home in a considerable amount of money. After the valuation, the lender offers an amount according to the current value of the property in the market. The age is also a significant factor to affect the final decision of the lender.

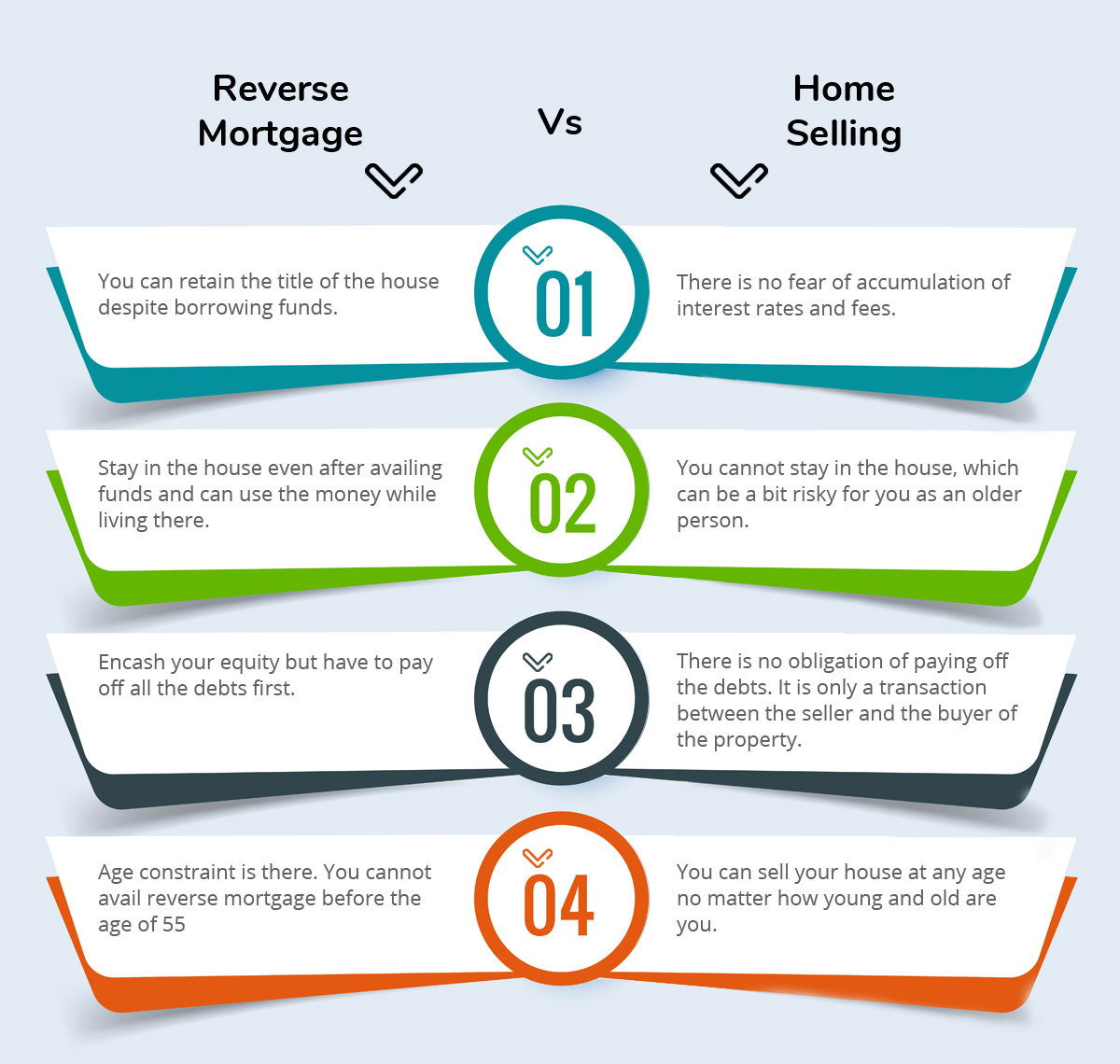

You can either borrow in a lump sum amount that is tax-free or can drawdown whenever required. There are no monthly repayments in a reverse mortgage, and the interest keeps adding in debt. The mortgage amount is paid at the end in two conditions 1) When the mortgagor dies 2) When the mortgagor shifts to a long-term care home.

Reverse mortgages are also called as lifetime mortgages. It is because there is no last limit to pay off the funds. The mortgage stays until the mortgagor dies or moves to a care home.

Who can apply for a reverse mortgage?

The reverse mortgage is designed to help the older people, and the minimum age to apply is 55 years. However, according to the lending policies of the varied lenders, this limit may increase. Some mortgage providers may set the limit to 60 as the least age to apply for the funds.

If you talk about the maximum age in which one can apply for this equity release mortgage, usually the mortgage lenders do not put any such limit. Some may have the last limit of 85 years; fewer go for 95 and very few go beyond this.

Is it possible to get a reverse mortgage in a poor credit situation?

Yes, you can apply for a reverse mortgage with bad credit due to the following reasons –

- In a reverse mortgage, there is no complication of monthly instalments, which means the lender has less to do with the repaying capacity of the borrower.

- The funds are offered on the equity, which naturally works as the security against any risk. There is no dependence on current income status.

- The mortgage is paid through the sale of the house when the borrower dies or move to a care home. It gives surety of the payment to the lender.

We can arrange the best deals on reverse mortgage despite your poor credit situation. We always advise our customers to keep a good recent financial behaviour. Bad credit is not a big obstacle in obtaining funds, but the recency of such issues is not good if you want to borrow a big amount.

How much can you borrow through a reverse mortgage?

It depends on the affordability rules set by the varied mortgage lenders. The amount that you can borrow depends on the factors of your age, health conditions (current and past) and value of the property. Usually, an older person can borrow more. If you apply at the age of 75, you can borrow a larger amount than an applicant who is 56 years old.

According to the age and home value, the borrowing limit and the interest rates get affected. Higher property value and older applicant brings a good deal with lower interest rates, and the LTV for reverse mortgages normally goes up to 55%. Few lending companies can consider you to provide a higher LTV according to your circumstances.

How much equity should you have for a reverse mortgage?

Usually, you must own at least 50% or more equity on your home. The lenders organize a home valuation of your house to know the actual value of the property. Naturally, lenders want you to pay off a considerable about of the existing mortgage (if you have) before applying for a reverse mortgage. It helps earn better equity and borrow a larger amount.

Pros and Cons of reverse mortgages

| Pros | Cons |

|---|---|

| An easier way to borrow funds without any worry of monthly instalments. | The interest rates and fees keep adding and increase the loan balance. |

| No effect on the ownership status, you can retain the title of the home. | After using the equity, it is difficult to leave as an asset to heirs. If you leave, they have to repay the loan balance. |

| Older adults near to the minimum age of 55 years cannot borrow a big amount as compared to the older ones. | The fee can be higher as compared to traditional mortgages. |

| You can borrow tax-free if you are taking a lump-sum amount. | Eligibility for benefits such as medical benefits, social security etc. may get affected. |

What are the major costs in the reverse mortgage?

The actual number and amount of costs depend on the lender and the type of platform; you use to get funds. The following are the main elements when it comes to the costs of a reverse mortgage in the uk.

- Legal costs

- Completion fee

- Property valuation

- Arrangement fee

You may also find the broker fee a part of the total cost, but not all brokers take payment. If you borrow through Shine Mortgages, there are no charges.

Can you buy a home with a reverse mortgage? YES!!

A reverse mortgage is like a tool to release the equity, and the amount you use can be used for any purpose. If you want to use the money for home buying, it is perfectly fine. Many people utilize the borrowed funds for the same purpose. They either partly or fully finance their property purchase through the funds obtained through a reverse mortgage.